BOOKS OF PRIME ENTRY

The Meaning of Books of Original Entry or Subsidiary Books

Give the meaning of books of original entry or subsidiary books

The ledger accounts of a business are the main source of information used to prepare the financial statements. However, if a business were to update theirledgers each time a transaction occurred, the ledger accounts would quickly become cluttered and errors might be made. This would also be a very time consuming process.

To avoid this complication, all transactions are initially recorded in a book of prime entry. This is a simple note of the transaction, the relevant customer/supplier and the amount of the transaction. It is, in essence, a long list of daily transactions.

The Functions of Books of Original Entry or Subsidiary Books

Identify the functions of books of original entry or subsidiary books

A Journal is an accounting record that is used to record the different types of transactions in chronological order or date order. Journals are often called or referred to as the books of original entry. The reason is that this is the first place that business transactions are formally recorded.You can think of a Journal as a Financial Diary.

Specialized Journalsare journals used to initially record special types of transactions such as sales and purchases. All these journals are designed to record special types of business transactions and post the totals accumulated in these journals to the General Ledger periodically (usually once a month).

The General Journal

The Journal is a textual record of events(Debit and Credit)that is characterized by the fact that all the records it contains are in a sequential chronological order. TheGeneral Journalis used to record unusual or infrequent types of transactions. Type of entries normally made in the general journal include depreciation entries, correcting entries, and adjusting and closing entries.

The Cash Book

TheCash Bookis used to record the receipt and payment of money by the business in the form of cash, or through the business bank account. It contains the cash and bank accounts.

Sales Journal

The Sales Journal is a special journal whereCredit sales to customersare recorded. Another name for this journal is the Sales Book or Sales Day Book.

Purchases Journal

The Purchases Journal is a special journal whereCredit purchases from customersare recorded. Another name for this journal is the Purchases Book or Purchases Day Book.

Returns Inwards Journal

TheReturns Inwards Journalis a special journal that is used to record the returns from debtors and allowances of goods sold on credit. Another name for this journal is the Sales Returns Book.

Returns Outwards Journal

TheReturns Outwards Journalis a special journal that is used to record the returns to creditors and allowances of goods purchased on credit. Another names for this journal is the Purchases Returns Book.

The Petty Cash Book

This is just a fancy name that describes a special fund that is set up and used for minor and unanticipated cash expenses where a cheque can’t be written or the amount is so small that you don’t want to write a cheque. The petty cash account is based on the Imprest System which is a system of cash disbursement, cash expenditure and reimbursement of that expenditure.

Several books of prime entry exist, each recording a different type of transaction:

| Book of prime entry | Transaction type |

| Sales day book | Credit sales |

| Purchases day book | Credit purchases |

| Sales returns day book | Returns of goods sold on credit |

| Purchases returns day book | Returns of goods bought on credit |

| Cash book | All bank transactions |

| Petty cash book | All small cash transactions |

| The journal | All transactions not recorded elsewhere |

Recording Business Transactions in the Books of Accounts and their Effects to Ledger Using Different Methods

Record business transactions in the books of accounts and their effects to ledger using different methods

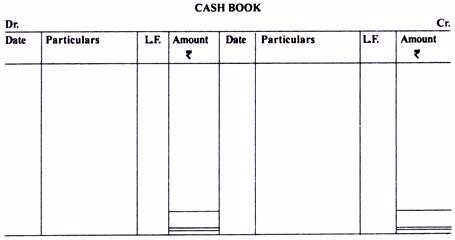

Types of Cash Books (With Specimen)

Here we detail about the three types of cash book, i.e., (1) Simple Cash Book, (2) Two Column Cash Book, and (3) Petty Cash Book.

Simple Cash Book:

Simple cash book contains only one amount column on each side (debit and credit) for recording cash receipts and cash payments.

A format of simple cash book is given below:

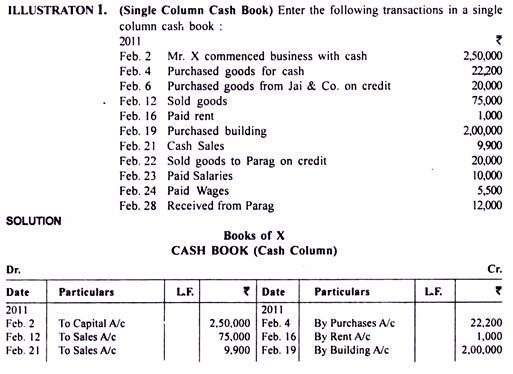

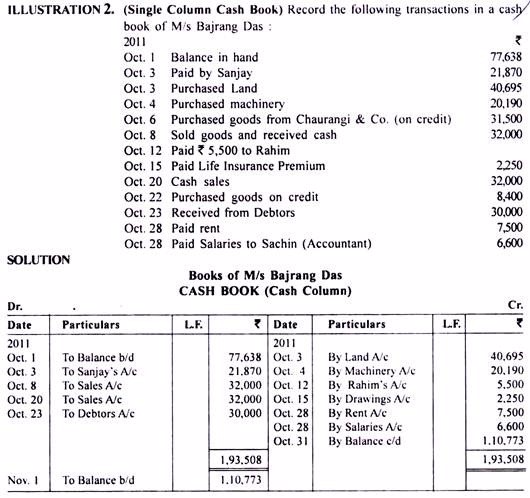

For recording transactions in the simple cash book, the foremost step is to understand the rule for recording transactions i.e., which account is to be debited and which account is to be credited.

Rules for Recording Transactions:

We know that cash book is also a cash account and there are two approaches for recording business transactions in the books of accounts. One is ‘Traditional Approach’ and the other is ‘Equation Based Approach.

Under traditional approach, cash is a real account so that following the rule: ‘Debit what comes in and credit what goes out’, receipt of cash is to be debited (i.e., cash comes in) in the cash book and payment of cash is to be credited (i.e., cash goes out).

Similarly, in the equation based approach, cash is an asset and following the rule: ‘Increase in asset is to be debited and decrease in asset is to be credited’, receipt of cash is debited (i.e., increase in cash) and payment of cash is to be credited (i.e., decrease in cash) in the cash book.

Procedure for Recording Transactions:

After knowing the rule for recording a transaction, it is essential for us to learn the procedure for recording the transactions in the simple cash book. It can be observed from the above format that the columns on ‘Receipts Side’ of the cash book are similar to the columns appearing on ‘Payment Side’.

However, for recording transactions in the cash book following steps should be taken:

Step 1:

- In the ‘Date’ column, the day, month and the year, on which transaction occurs should be recorded.

Step 2:

- In the ‘Particular’ column, the nomenclature of the accounts, from where cash is received or paid, gets recorded.

Step 3:

- In the ‘L.F.’ (Ledger Folio) column, the folio (page number) of the respective ledger, where the posting of the transaction is made, shall be recorded.

Step 4:

- In the ‘Amount’ column, the actual cash paid or received is recorded.

Step 5:

- The last, but not the least, cash book is to be balanced. As already stated, a separate cash account in ledger is not opened when a cash book is maintained. Like an account is balanced in the ledger, the cash book is balanced in the same way. Depending upon the need and size of the enterprise, the cash book should be balanced daily, weekly or monthly.

Total of the ‘Amount’ column on both sides of the cash book is compared and the difference if any, should be entered on the credit side of the cash book under the ‘Particulars’ column as “By Balance c/d’. By putting the difference under the amount column both sides of the cash book become equal.

Now total amount under the ‘Amount’ columns on both side of the cash book is written opposite to each other. The closing balance shown as ‘By Balance c/d’ becomes the opening balance for the next period and is written as ‘To Balance b/d’. opening balance for the next period and is written as ‘To Balance b/d’.

Example;

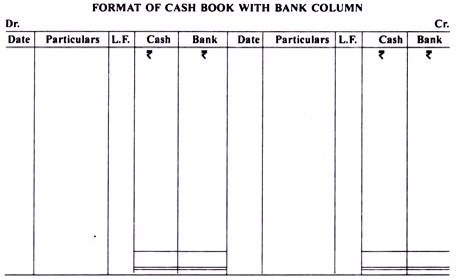

TWO Column Cash Book- Cash Book with Bank Column:

Simple cash book with single amount column on either side is maintained if the organization has only cash transactions. However, due to security and legal bindings, sometimes the transactions have to be necessarily routed through banks. The receipt issued by the cashier is the source document for cash receipts.

Any document viz., invoice, bill receipt etc., through which payment has been made, will serve as a source document for payment. These documents, popularly known as vouchers are numbered serially and filed in a separate file for future reference, verification and audit.

Bank facilitates a business enterprise to open current account in which the business enterprise can withdraw amount in excess of what is available in the current account. In that case transactions related to cash and banks are to be recorded separately in a cash book so that at any particular period of time, cash balance available in the cash chest and bank balance available in the bank account can be known immediately.

It is better to record transactions relating to both cash and bank in the same cash book. For this purpose, one more amount column for recording bank transaction is to be added on both sides of the cash book. This is known as bank column. Under bank column of the cash book, cash transactions routed through bank are recorded.

A format of cash book with bank column is given below: A format of cash book with bank column is given below:

Similar to simple cash book, cash transactions are recorded in the two column cash book. The difference is that here we also record banking transactions i.e., the transactions in which bank is also involved.

Rule for Recording Transactions:

Entries in the cash column are recorded similar to recording transactions in the simple cash book. For recording bank transactions there are two approaches. One is ‘Traditional Approach’ and the other is ‘Equation Based Approach’. Under traditional approach, bank is personal account so that as per the rule: ‘Debit the receiver and credit the giver’, receipt of cash by the bank is to be debited (i.e., debit the receiver) in the cash book and payment of cash by the bank is to be credited (i.e., credit the giver).

However, in the equation based approach, bank is an asset and the rule: ‘Increase in asset is to be debited and decrease in asset is to be credited’, will be followed. If in a transaction, bank column increases, bank column of the cash book is to be debited (i.e., increase in bank) and decrease in bank column is to be credited (i.e., decrease in bank) in the cash book.

Procedure for Recording Transactions:

The procedure for recording transactions in the cash book with bank column is the same as that stated in the case of simple cash book. Depending upon the reputation or goodwill of the business enterprise, bank fixes a limit on withdrawals, which is known as credit limit. It means bank column may either show debit or credit balance depending upon how receipts and payments made through bank column of the cash book have affected the credit limit.

Difference between General Ledger and Purchase Ledger and Sales Ledger as Applies by Businessmen

Distinguish General ledger from purchase ledger and sales Ledger as applies by businessmen

A general ledger is a company's set of numbered accounts for itsaccounting records. The ledger provides a complete record of financial transactions over the life of the company. The ledger holds account information that is needed to preparefinancial statementsand includes accounts for assets,liabilities, owners' equity, revenues and expenses.

ThePurchase Ledgeris your record of yourpurchasesand expenses, whether or not you have paid them and how much you still owe. On a Balance Sheet, the total unpaid bills will usually will be called Trade Creditors or Accounts Payable. ThePurchase Ledgerhas an Account for every Supplier.

- READ TOPIC 2: Petty Cash And Impress System ( Column Petty Cash Book)

No comments:

Post a Comment