The subject matter tells us about what we study in Economics. However for the sake of conveniences, economics is concerned with the following:

1. It is concerned with how human being earns their living through exchange i.e. it is concerned with how man employs scarce resources to satisfy material wants.

2. It deals with production, distribution, exchange and consumption of goods and services.

3. It also deals with human activities which involve selling and buying. It doesn’t deal with goods and services that man produces for the sake of self-satisfaction.

These goods and services must have exchange value a part from satisfying human wants.

Is a process of rewarding or making payment to the factors of production such as Land -Rent, Labour- Wages, capital-Interest and Entrepreneur-Profits.

This refers to human desires.

-The resources used to satisfy the wants are (limited in number) scarce.

-Human wants can be satisfied by alternative means, E.g. rel="noopener" target="_blank">Thirstycan be quenched by drinking water or soft drinks.

-Human wants are complementary.eg; Driving is satisfied by car and fuel.

Are those necessary things when you loose it can cause death(Basics needs such as food,shelter and clothes).

Refers to the inputs which are needed to produce goods and services. They are also known as the factors of production or means of production. The factors of production are things which are necessary for production.

Refers to the total expenditure by households or final users on goods and services which yield utility in the current period OR

Is the process of using goods and services to satisfy wants.

Are things that are produced by the factors of production like land, labor, capital etc. and are consumed by man to satisfy his wants. It involves goods and services.

Is a creation of goods and services for personal consumption or use.

Is a process of making goods and provision of services to satisfy people’s needs or wants e.g. Giving crops for food, building houses.

Refers to the country’s stock of resources and goods that can be used to satisfy wants.

A country’s wealth consists of stock of resources and goods that can be used to satisfy wants. It includes; machines, buildings, and human skills.

Refers to the tangible things which satisfy human wants.

Refers to the level of satisfaction that a person or group of people derives from the consumption of goods and services.

The study of the impact of the pattern of resources allocation on society’s well being(or welfare)

(a) the methods of production

(b) the type and quantity of goods and services produced and consumed

(c) the relative share of goods and service going to each household, are satisfactory.

Pareto efficiency–a situation in which it is not possible to make someone better off without making someone else worse off.

Equity is concerned with the treatment of different individuals or groups in society.

Exist when the price and quantity of a commodity match both consumers and producers.

In this case the quantity demanded and supplied are equal and the market clear.

Exist when the price and quantity of commodity fail to match consumers and producers expectation.

These are things which can satisfy human wants like clothes, cars, houses etc.

These are goods which are provided freely by nature. E.g. Air, sunshine, rainfall, ocean water and forest.

These are the goods produced by human efforts and posses the following qualities;

i. They have utility, i.e. ability to satisfy wants/needs.

ii. They have exchange value, i.e. they can be bought or sold.

iii. They are transferable in terms of ownership from one person to another person.

Thus Economics is concerned with economic goods and not free goods because production in Economics is for exchange for which the economic goods possess value.

Consumer Goods – These are goods produced for final consumption or use such as food, radio, clothes, furniture etc.

Producer Goods – These are goods which are produced to assist in the production of other goods. They are also known as capital goods. Producer goods include; machinery, raw material, workshop, building etc.

Perishable Goods : These are goods which can easily be destroyed or spoil like food stuffs e.g., milk, meal, fruits, vegetable etc.

Durable Goods: These are goods which can last or stay for a long period of time without being destroyed or damaged such as buildings, machines, furniture etc.

Private goods: Are goods owned by individuals for example private car, clothes, houses etc.

Public goods: Are goods owned and enjoyed by all individuals in the country. For example; roads, defense etc.

Feature of Public Goods:-Non divisibility i.e., provided in totality to the public.

Non rivalry i.e., there is no competition of consumption. One person can consume extra units without reducing consumption of others.

Intermediate goods:– Are goods in progress e.g. raw material.

Final goods:– Are goods ready for consumption.

Normal Goods:– Are the goods for which their demand increases when the real income of the consumers increases while their demand decreases when income of consumers decreases.

Inferior Goods:- Are goods which the demand of the goods by the consumers decreases when real income increases.

PRODUCTION

Is a creation of goods and services for personal consumption or use.

OR

Economists define production as a process of creating goods and services for exchange i.e for sale in order to satisfy people’s needs.

OR

Is a creation of utility. Utility means the level of

satisfaction a consumer derives from consuming a certain unit of goods

and services.

Economics Activities:

Prof. Marshall defined all activities concerning with the earning and spending income (wealth) such as-; the activities of farmers, labor, shopkeeper, teachers, doctors and advocates.

Thus all activities which are done with view to earn income are called Economic activities.

NON ECONOMIC ACTIVITIES

Refers to all activities which do not have the earning of wealth as their nature. E.g. .playing football for health reasons, singing by mothers, teachings by a teacher to his own children, etc.

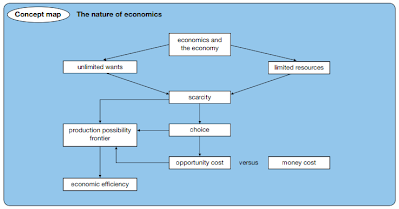

SCARCITY

Means limited in supply or less than that what is required or needed.

CAUSES OF SCARCITY.

Limited stock of resources.

Resources are limited in number therefore it is not possible to produce enough goods and services to satisfy all wants.

Unlimited wants.

Wants are unlimited in number therefore resources available cannot produce enough goods and services to satisfy all wants.

Alternative uses of the available resources.

E.g, same land can be used to grow beans, rice or other uses such as land for construction of buildings.

Resources are normally scarce and therefore you have to choose from the few alternatives to satisfy the needs.

Producers – chooses what goods to produce.

Consumers – Decides which wants/needs they require.

SCALE OF PREFERENCE

Is a list of all wants in an order to their importance such that that the most important wants are kept first on the list followed by the less important wants.

OPPORTUNITY COST.

The true cost of producing an additional of goods or services in their value of goods or services that must be given up to obtain. E.g. A student may have two alternatives of her/his evening time to do homework and the alternative is to play football.

If he/she chooses to play football, the opportunity cost of playing football is the homework.

EXCHANGE

Refers to the process of selling or buying of goods and services to government to guarantee wealth (income).

MORE IMPORTANCE TO WEALTH DEFINITION

The definition gave too much importance of wealth and ignored human welfare and moral values. Because of these weaknesses, Adam smith’s definition of economics could not be accepted.

WELFARE DEFINITION

According to Marshall in his book titled “principle of Economics”. Defined economics is the study of man in ordinary business of life. It examines that part of individual and social actions which is closely connected with the attainment and the use of material requisites for well being.

The main features of Marshall’s definitions are:

Economics is a social science and it studies the economic activities of social normal and real man.

Wealth is a means while the ends are human welfare i.e. wealth is for man and man not for wealth.

The central point in the study of Economics is man’s material welfare.

CRITICISM

Strongest attack on Marshall’s Definition comes from Prof. Robbins.

The main criticisms of Marshall’s definition are;

Wrong concept of material goods. Economics is not all about the study of material goods. In reality it is not easy to distinguish material things and immaterial things. Economics also studies immaterial goods such as the services of teachers, doctor, advocates, singer etc.

Economics has no relationship with the material welfare according to Prof. Robbins. Economics can’t be linked with material welfare it is because;

The concept of welfare cannot be defined exactly.

In economics we study a number of such activities which cannot be regarded goods from welfare point of view E.g. war, production of home etc.

Economics do not have appropriate scale of measurement by which welfare can be measured.

Not a social science.

According to Robbins, Economic is not a social science rather it is a human science.

Wrong division of human activities in Economics.

Marshall Division of human activities was also wrong. According to Robbins every activity has main aspects and one of them is economic aspect.

Classification – Marshall Definition is classified. There are many categories but the destination between there is not clear Eg ordinary business, social and unsocial, material and immaterial, economic and non-Economic etc.

Marshall’s definition was better than Adam smith’s definition yet was rejected after sometimes because of these weaknesses.

Welfare Definition

Lionel Robbins published a book “An Essay on the Nature and Significance of Economic Science” in 1932. According to him, “economics is a science which studies human behaviour as a relationship between ends and scarce means which

have alternative uses”.

The major features of Robbins’ definition are as follows:

a) Ends refer to human wants. Human beings have unlimited number of wants.

b) Resources or means, on the other hand, are limited or scarce in supply. There is scarcity of a commodity, if its demand is greater than its supply. In other words, the scarcity of a commodity is to be considered only in relation to its demand.

c) The scarce means are capable of having alternative uses. Hence, anyone will choose the resource that will satisfy his particular want. Thus, economics, according to Robbins, is a science of choice.

Criticism:

a) Robbins does not make any distinction between goods conducive to human welfare and goods that are not conducive to human welfare. In the production of rice and alcoholic drink, scarce resources are used.

But the production of rice promotes human welfare while production of alcoholic drinks is not conducive to human welfare. However, Robbins concludes that economics is neutral between ends.

b) In economics, we not only study the micro economic aspects like how resources are allocated and how price is determined, but we also study the macro economic aspect like how national income is generated. But, Robbins has reduced economics merely to theory of resource allocation.

c) Robbins definition does not cover the theory of economic growth and

development.

SCARCITY DEFINITION.

According to Lionel Robbins and his followers like Stigley, Samuelson, Carnations and many other. Modern Economists defined economics as;

A science which studies human behavior as a relationship between ends and scarce means which have alternative uses.

FACTS OF ROBBIN’S DEFINITION.

According to Robbin’s and his follower Samuelson.

- Human wants are unlimited.

- Human wants have alternatives.

- Resources are scarce.

- Resources have different importance.

The unlimited wants and the scarcity of the resources give rise to the problem of choice.

Choice refers to the process of making selections among multiple or several alternatives.

CRITICISM OF ROBBIN’S DEFINITION

The difference between means and ends is not clear. This definition uses two terms, means and ends which have not been clearly distinguished.

Neutral towards ends.

The definition regards economics is neutral towards ends if it is occupied then used. The study or economics would be of no use of which it would not remain a fruitfully science. Thus economist is a tool maker as well as toll users.

Reduced merely to valuation theory.

Robbins definition has reduced Economics merely to evaluation theory. This does not taken into account. The problem of macro economics and growth.

Problem of abundance.

All economic problems do not arise from scarcity. Some of them may also arise from abundance, such as the problem of over production etc.

Hence in simple words we can say Economics is a science that studies human behavior as a relationship between ends and scarce means which have alternative uses.

i) Wealth Definition

Adam smith (1723 -1790), in his book “An Inquiry into Nature and Causes of Wealth of Nations” (1776) defined economics as the science of wealth. He explained how a nation’s wealth is created.

He considered that the individual in the society wants to promote only his own gain and in this, he is led by an “invisible hand” to promote the interests of the society though he has no real intention to promote the society’s interests.

Criticism

Smith defined economics only in terms of wealth and not in terms of human welfare. Ruskin and Carlyle condemned economics as a ‘dismal science’, as it taught selfishness which was against ethics.

However, now, wealth is considered only to be a mean to end, the end being the human welfare. Hence, wealth definition was rejected and the emphasis was shifted from ‘wealth’ to

‘welfare’.

ii) Growth Definition

Paul Samuelson defined economics as “the study of how men and

society choose, with or without the use of money, to employ scarce productive resources which could have alternative uses, to produce various commodities over time, and distribute them for consumption, now and in the future among various people and groups of society”.

The major implications of this definition are as follows:

a) Samuelson has made his definition dynamic by including the element of time in it. Therefore, it covers the theory of economic growth.

b) Samuelson stressed the problem of scarcity of means in relation to unlimited ends. Not only the means are scarce, but they could also be put to alternative uses.

c) The definition covers various aspects like production, distribution and consumption. Of all the definitions discussed above, the ‘growth’ definition stated by

Samuelson appears to be the most satisfactory. However, in modern economics, the subject matter of economics is divided into main parts, viz., ) Micro Economics and ii) Macro Economics.

Economics is, therefore, rightly considered as the study of allocation of scarce resources (in relation to unlimited ends) and of determinants of income, output, employment and economic growth.

GENERAL MEANING OF ECONOMICS.

Is a social science which studies how societies allocate scarce resources in production of goods and services to satisfy their needs.

IMPORTANCE OF STUDYING ECONOMICS.

1. It helps to build up a body of principle and furnish the economist with lots of economic analyzing that will enable students to understand current economic problem and to see the economics consequence of perusing a particular time of policy.

2. It helps in interpreting economic issues rising from government and non-government policies.

3. It helps in managing personal life and that of the society.

4. It helps to distinguish various economic systems such as capitalist, socialist and mixed economy.

5. It explains economic theories and shows how they apply to a particular economy. Economic theories are simplified representation of the real word that we use to understand, explain and predict economic phenomena in the real world. They can be inform of statements or graphs.

6. Helps in discussion and analysis of international economic issues and dealing.

7. It helps students to use the terminologies, language and symbolism of the subject clearly and communicate economic ideals.

BRANCHES OF ECONOMICS.

There are two main branches of Economics.

- Micro-economics

- Macro-economics.

MICRO ECONOMICS.

Micro means small. Micro economics refers to a branch of economics which studies the behavior of individual economic units such as; price determination of a commodity (goods), behavior of consumers or producers (firms) etc.

Micro economics is also termed as the price theory. Micro economics also deals with;

- Price determination in the market.

- How a product is made by the firm (individual) producer.

- How income is distributed.

- How wages, interest, rent and profits are determined.

IMPORTANCE OF MICRO ECONOMICS

1. Helps in explaining the functioning of the free enterprises economy. The working of capital economy is based on micro economics.

2. It tells us how consumers and producers make decisions on how to allocate their limited (scarce) resources. They use the marginal approach to determine the part they will gain more.

3. It helps in determination of prices of various commodities in the market.

4. It explains the conditions for efficiency for both production and consumption.

MACRO ECONOMICS.

Macro means large. Macro economics analyzes economic problems on national or aggregate basis. Macro economics is also known as the income theory.

Therefore Macro economics is a branch of economics which deals with the studies of aggregation and overall performance of the economy such as;

- Total consumption.

- Total employment.

- National income.

- General Price level.

- Consumer price index (CPI).

- Total savings etc.

It addresses issues like the relationship between inflation and unemployment, effects of deficit in the balance of payment, relationship between money supply and general price level.

Thus for comprehensive economic analyze both micro and macro approaches must be adapted.

IMPORTANCE OF MACRO ECONOMICS.

1. Useful in understanding the functions of complicated economic systems such as the Command economy system.

2. Useful in the formulation of various economics polices in the country such as the taxation policy.

3. It helps to provide solutions to urgent economic problems facing the economy such inflation, unemployment.

DEVELOPMENT OF ECONOMICS

It studies the principles and problems concerning economic development of the country.

ECONOMIC LAWS

There are economic statements which show the relationship between economic variables. It shows that a certain thing happens under given economic conditions. It regulates relationship in main economic activities of production, exchange, consumption and distribution.

Lionel Robbins defined economic laws as a statement of uniformity which govern human behavior concerning utilization of resources for achieving of unlimited ends. Example of economic laws is laws of demand and supply.

Therefore economic laws shows tendencies of what happens under given economic conditions thus they express people’s reaction to economic forces Eg In the example about the laws of demand show that consumer tend to buy more as the price of commodity decreases and suppliers tend to supply more when the price of commodity increase.

Sometimes people believe contrary to the laws e.g under given conditions of exceptional demand people with low income demand more inferior goods at higher price that at lower price.

CHARACTERISTICS OF ECONOMIC LAWS.

They are not static i.e. they change with time and economic conditions.

They are hypothetical i.e. they are based on assumptions.

CLASSIFICATION OF ECONOMIC LAWS

Pure and Natural laws.

These emerged purely from interaction of economic variables such as price and quantity demanded as supply scarcity and choice etc.

These laws can operate in all economic systems. E.g. the laws of demand and supply and the law of diminishing marginal utility.

Law of super structure (Government or state law).

These are laws provided by the government or state to regulate or control economic activities. E.g. law of taxation, law of controlling consumption of certain commodities. Law of stabilizing the economy etc.

Law of specific economic system.

These are the laws specific to a certain economic system and they control relationship among the people in the process of production, consumption distribution, exchange once a system is replaced by the new system. E.g of specific laws is;

- Laws of private ownership of means of production.

- Laws of public ownership of major means of production.

General laws.

These are laws which operate in all economic systems whether socialist or capitalist E.g. Demand and supply.

IMPORTANCE OF ECONOMIC LAWS.

Guide economic events and serve as a basis for the formulation and evaluation of economic policies Eg the law of demand and supply. Help the tax authority to fix a rate that will not cause a big increase on price.

They are useful in planning process ie planner can forecast implication of various plans by using economic laws of what will happen in production if domestic industries are given subsidizing.

FUNDAMENTAL ECONOMIC PROBLEMS.

The main central economic problem is the scarcity of resources in relation to unlimited wants.

There are sources of basic economic problems which exist in societies needed to confident three inter-related questions. These are;

What to produce.

It is related with the types (ranges) and quantity of goods to produce. Since resources are scarce, we must choose between different alternative collection of goods and services that may be produced.

It also involves the allocation of resources between different types of goods. For example, consumer goods and producer goods .

The decision to this question is unanswered. Differently under capitalist economy it is answered by price mechanism while in planned socialist t is determined by central planning authority and also by mixed economy.

How to produce.

This question arise from the basic economic problem that since resources are scarce in relation to unlimited wants, we need to consider how resources are used that the best outcome may arise.

The question requires the determination of the method or techniques, the choice of the techniques of production will depend on the Efficiency and the price of factors of production i.e. the cost of production.

For whom to produce.

Since we cannot satisfy all the wants of all the population, decisions have to be taken concerning how many of each person’s want are to be satisfied i.e. it involves who should get how much. However the distribution will depend on the economic system of socialist, capitalist economic system.

In some economies the deliberate attempt to create policies that re-distributes wealth and income from rich to poor. This could be through the adaption of progressive taxation system.

In other economies there are no such policies and qualities of wealth and income usually based up on inheritance remain extreme.

Answering this question moral aspect of decision making become important.

Where to produce.

The producer has to make decision regarding the place where the firm has to be located. The location of the firm depends on the;-

- Availability of the means of transport and communication, power and water supply.

- Supply of labor.

- Availability of banks, hotels, schools, and hospitals etc.

When to produce.

A producer must also decide the right time to produce a given commodity.

How much to produce.

It relates to mankind decision regarding the quantity or amount of the commodity to be produced.

The answer to the above problem is determined by different economic systems.

- In socialist economy, the use of central planning authority.

- In capitalist economy, the use of price mechanism.

- In mixed economy, the use of both methods.

SCARCITY AND CHOICE

Other decisions on economic problems centers round the two basic concepts, scarcity is useful to understand them more clearly.

Scarcity: – The scarcity implies limitlessness in supply therefore; when we say the resources of a country are scarce it means that the resources are limited in supply.

A resource is said to be scarce when there isn’t enough of it to satisfy all the people’s wants, but if;

Economic goods and services are scarce in the sense that is not available in sufficient of zero prices. If something is so abundant that we can have all we want without paying for it is not a scarce commodity e.g. Air under ordinary circumstance is not scarce.

Economic goods and services are scarce relatively to the people’s desires for them.e.g. There are more good bananas than bad banana, but it is good bananas which are scarce because it is the good one which people desire to consume.

The scarcity of economic goods and services arises from scarcity of resources such as land, labor, capital and entrepreneur used to produce them.

NOTE

Regarding the problem of scarcity we must be very clear in our minds that it is found in all countries whether it may be poor or rich country. However the form scarcity here is used in relative sense of resources is limited in relation to man’s wants. In this sense if it is true for a rich and developed country thus scarcity is a fundamental problem and universal in nature.

Because of scarcity in resources, we must choose from among the many wants and whenever we choose we must force go satisfying. Some economists defined economics as a study of how people choose to use their scarce resources in attempt to satisfy their unlimited wants.

Since there are insufficient productive resources in the world, therefore man is left to find the solution to that problem and the first option is to economize, that is to make the best and efficient use of the resources available without any wastage.

A SCALE OF PREFERENCE

Is a sort of list of all unsatisfied wants arranged in the order of importance. In the scale of preference the most pressing wants are placed on top while the less pressing wants are placed at the bottom.

OPPORTUNITY COST

If has been observed that in reality, scarcity leads to the problem of choice and once we choose we must go without others.

Satisfaction of one’s must involve foregoing something else. Therefore the opportunity cost of real cost of satisfying any wants is the alternative that has to be foregone in order to do so.

That is the real cost of satisfying anything in the alternative that has to be forgone. In simple language opportunity cost is the sacrificed alternative in deciding to do one thing and not the other.

Human wants are unlimited while the means to satisfy them are limited. Therefore one has to choose what want to satisfy because one cannot satisfy all wants due to scarcity of resources.

Usually one satisfies the most pressing wants before satisfying the less pressing wants.

The sacrificed goods are thus the real cost or opportunity cost of satisfying the wants that are sacrificed.

E.g. If you had to choose between leisure and work, sacrificing leisure then the real cost or opportunity cost is very useful in the process of planning especially in the question of resources allocation. When we choose to allocate more resources to production of consumer goods we are necessarily forced to the reduce the allocation of resources to the production of producer/ investment goods.

PRODUCTION POSSIBILITY FRONTIER OR CURVE (PPF OR PPC)

A production possibility curve is a curve representing all possible combinations of total output that could be produced by the economy when its resources were fully and efficiently utilized under a given state of technology.

The production possibility curve is also known to other economist as production possibility frontier or Boundary.

The concept of production possibility curve helps to explain the concept of scarcity and opportunity cost.

The following are the assumptions of the production possibility curve;

- The resources are fully and efficiently utilized.

- There is a constant state of technology.

- Only two commodities are being produced.

- The amount of resources is fixed.

Given that the resources and technology are fixed, we can produce more of every commodity from the resources which can be used to produce more of another commodity.

In the production possibility curve, since the resources are scarce, we are forced to choose between production of capital goods and consumer goods. Sacrificing the production of consumer goods. Thus the opportunity cost of more capital goods is the consumer goods that we have to sacrifice.

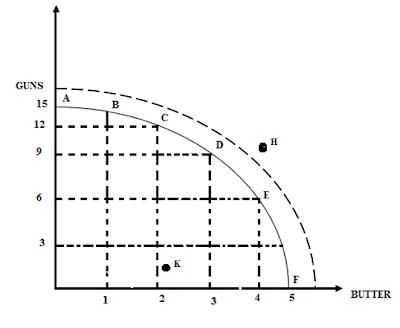

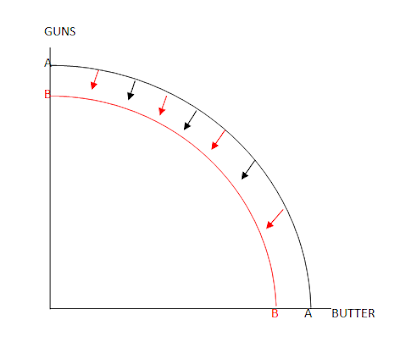

GRAPH OF PRODUCTION POSSIBILITY CURVE

From the graph, we learn that the shape of the production possibility curve is concave to the origin. Because there must be the decrease in output of guns in order to add more unit of butter e.g. To produce one unit of butter we have to fore got one unit of gun i.e. from A to B.

This is called the marginal rate of technique substitution of butter for gun and it goes on increasing.

If the economy devoted all its resources to the production of gun it can produce 15 thousand guns but the production of butter will be zero.

Therefore if we decide to produce 1unit of butter we have to produce 14 units of guns.

From the graph therefore we learn that if butter we want to produce more butter we have to reduce the output of guns and vice verse i.e. we can transform guns into butter or butter into guns.

The point on the boundary of PPC i.e. A, B, C, D, E and F represents the combination of goods that can be produced using the country’s available resources and technology.

Any point inside the boundary say K is one from the diagram it shows inefficiency of which may be under utilization or unemployment of the countries resources.

From point A to point F, it indicates the increase in the production capacity of the economy. The new graph tells us that economy can now produce large quantity of output.

Point H on the graph indicates unattained point of which it is outside the PPC .point K will be attained when the economy increases its production leading to the shift of the PPC from its original position to point K.

How choice, opportunity cost and scarcity are shown on the PPC.

Choice is indicated by selecting any point on the PPF. When resources are fully utilized i.e. a,b, c,d,e and f.

Opportunity cost is indicated by movement along the PPF i.e. a, b, c, d, e and f. e.g. The opportunity cost of producing 15 units of guns is the 0 unit of butter that you forego at full employment of the resources.

Scarcity is indicated by point H which has not been attained. It will depend on the expansion of the production in the economy.

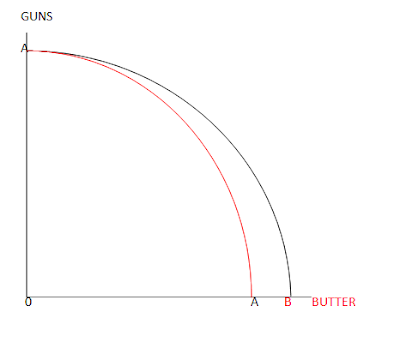

In order to move the economy from the current production possibility curve to the outer production possibility curve, the economy has to;-

Increase in the stock of its resources.i.e. To increase the quality of labor, land, capital and entrepreneurship.

Improve the state of the technology to more advanced methods in order to find move output of maximum cost of production of capital.

DIAGRAM FOR INNOVATION OF NEW RESOURCES

In some other cases the PPC curve tends to shift inwards, this signifies the decline of the economy which may be due to;-

Exhaustion of the economy’s natural resources such as land.

Working population is falling.

Technology available was changed.

Underemployment of the resources of a country of which some of the resources are left idle.

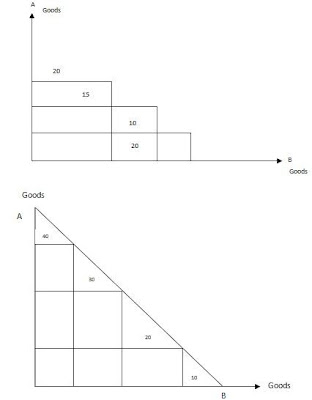

SHAPES OF PRODUCTION POSSIBILITY CURVE

The graph is concave to the origin due to the law of diminishing return, as resources are transformed from goods A to goods B the extra out of B becomes successively smaller while the amount being sacrificed in A becomes large and large.

Amount sacrificed for one good and gained by the other is constant represented by a straight line.

Features of production possibility curve

- Two commodities involve.

- There is fixed technology.

- Full employment and productive efficiency.

- Fixed resources.

- Perfect factor substitution.

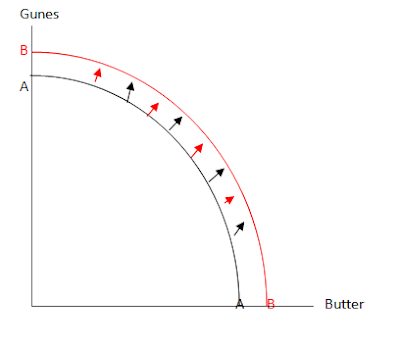

SHIFTS IN PRODUCTION POSSIBILITY CURVES

An economy’s production potential is

constant changing.The Production possibility curve (ppc) will shift

outward to the right because capacity to produce goods and services

increases as shown below

PPC INWARD TO THE LEFT as shown below:-

PPC curve shift to the left because economy’s production potential

declines.This could occur due to the war or natural disaster which

reduces a countries resources.

A CHANGES IN THE SLOPE OF THE PRODUCTION POSSIBILITY CURVE (PPC)

example improvement of production technique in manufacture.

ECONOMICS RELATED TO OTHER SOCIAL SCIENCE

The economist of today is indebted to the historian of the part history. I.e. in this sense that they supplied material of the formulation of economics conclusion.

1. ECONOMICS AND HISTORY

The economist of today indebted to the historian of the part history i.e. the sense that they supplied material of the formulation of economics conclusion.

Economists also can verify the correction of the old theory by comparing facts of the past and present.

Economists like Malthus used history methods to explain his theory of production.

No historian can have a rough knowledge of history of a country if he does not study its economic condition from this sense. Therefore economics without history has no root and without economics it has no fruits.

2. ECONOMICS AND PSYCHOLOGY

Psychology is that science of mind that it does with mental phenomena. Economics is the study of certain types of human behavior. Since behavior is conditioned by the mind, economics is related to psychology.

Wants, efforts and satisfactions which force the subject matter of economics are also mental phenomena e.g. The law of demand and supply are based on human behavior /psychology

3. ECONOMICS AND ETHICS

Ethics is a science proper or right conductor. It prescribes the moral code of behavior and it is concerned with what might be?

The ethical standard of the people of a country is influenced by some extended economic condition, for example; the decision on which taxes to impose and which scheme to spend government money deceive their inspiration from morals of the society.

Economic as system that institutional arrangement.

4. ECONOMIC SYSTEM

Economic system is that an institutional arranged where by human and natural resources of an economy cooperate with each other to produce goods and service.

OR

Is a set of institution which a society decides what, how and for whom to produce. It is a framework theory which a society allocates scarce resources among competition uses or it is an allocate mechanism of the society.

OBJECTIVES / FUNCTIONS OF AN ECONOMIC SYSTEM

1. To distribute output among the members of the societies and it must answer the question of who gets from the production of output.

2. Allocation of the resources i.e. every system is responsible for the allocation of resources for production of goods and services.

3. To provide maintenance and expansion of capital goods. Every system must expand capital goods.

4. To adjust production and consumption i.e. to make sure production does not exceed consumption and vice verse.

5. To make social choice i.e. to decide on behalf of the government what kind of goods and services to produce.

TYPES OF ECONOMIC SYSTEM

There are three main types of economics system;-

- Socialist economic system.

- Capitalist economic system.

- Mixed economic system.

SOCIALIST ECONOMIC SYSTEM

Command or socialist economic system is a type of economic system in which all major means of production are owned by the state.

FEATURES OF THE SOCIALIST OR COMMAND ECONOMY

1. Collective ownership. All major means of production such as factories, banks, schools hospital, and farms e.t.c are owned by state.

2. All economic decisions are made by the state. Economic decisions about what to produce, how to produce and to whom to produce are made by the country planning authority.

3. Exploitation is minimized and classes are not in extent. Profit is shared equally among the members and classes do not exist because wealth in the socialist economy is owned equally by all members.

4. Lack of freedom. In command economy producers are not free to make decisions on the allocation of scarce resources. What is to be produced is determined by the state consumers; likewise producers are not free on what goods and services to produce to the consumers.

5. There is equality among the members in a command economy. Majority of people have access to the national output as the state ensures equality in the distribution of wealth.

6. Low quantity and quality of outputs due to lack of competition.

7. Production is mainly gearing at maximizing utility of the society.

ADVANTAGES OF COMMAND ECONOMIC SYSTEM

It promotes welfare of the majority.

Under this system the government ensures achievement of minimum standard of living for the members of the society by using different approaches like;- provision of the free social subsidies etc.

Wastage of resources is minimized.

Proper planning on the allocation of resources ensures efficiency and full utilization of the resources.

Greater ability to tackle externalizes i.e. environmental pollution should be tackled into account when deciding up on the patterns of production. Command economy can easily deal with harmful effects of production activities.

There is no exploitation between people hence there is harmonious relationship between them.

The system is able to minimize inequalities in the distribution of income and wealth unlike the market economy.

Economic and social crises can be avoided. Since a command economy is planned, the government is able to control various macro-economics variables like money supply, investment, consumption, expenditure, tax etc.

This economic crisis such as inflation, recession, depression, unemployment, e.t.c can be avoided.

DISADVANTAGES OF COMMAND ECONOMIC SYSTEM

1. Lack of freedom of choice.

Under this system, freedom by producers and consumers over what to consume and produce are very limited.

2. Discourage individual efforts or ineffectiveness to work due to lack of private gains.

3.Inefficiency in production the system is characterized in

efficiency due to lack of competition low technology.bureaucratic

decisions, corruption, poor planning, too much protectionism to domestic

industries

etc.

4. Information cost of gathering information about what, how, for whom to produce is likely to be very high as it requires experts, planners, administrators and engineers etc.

5. Difficult in estimating demand without price sign us to estimate existing and future pattern of demand for goods and services becomes difficult.

NB

Socialism is still one of the economic system that today is practiced in Cuba, North Korea and China.

II. CAPITALIST ECONOMIC SYSTEM

The system is also known as market economy, unplanned or free enterprise economy. Capitalist economic system refers to the type of economic system in which all major means of production are owned by individuals and privates companies, with little government intervention. Examples of the countries which practice this system are USA, UK, Germany, France etc.

FEATURES OF CAPITALIST SYSTEM

There is private ownership of the major means of production such as land and capital.

There is freedom of choice. That is producers and consumers can make decisions on what, where and for whom to produce and consume.

Production is aimed at profit maximization i.e. for self interest resources.

Reliance and price mechanism as a means of allocating resources. Under capitalist economy all problems of what is to be produced where to produce and for whom to produce are answered by the price mechanism.

There is limited role by the government.i.e the government has little intervention over the allocation of the economic resources.

Competition. Under capitalist economy there is free entry of firms in production. These firms compete for resources and market. Such competition results to the increase in efficiency in production.

There is existence of classes. Under this system the society is divided into classes. That is the class of haves and have not i.e. the haves are those who own the major means of production and they have not are those who do not own the major means of production.

ADVANTAGES OF CAPITALIST ECONOMIC SYSTEM

Greater freedom of choice (consumer sovereignty).

This means that consumers are seeking to maximize their utilities, having the freedom to make choices from wider range of goods and services.

Competition may result into the increased efficiency in production i.e. to produce goods of high quality to win the competition.

Low burden to the government.

In this system, the government takes very few responsibilities in the provision of essential services.

High private initiatives. There are high motives to produce by private producers because of private profit, freedom of ownership and freedom of production.

Proper allocation of the resources.

Price mechanism eliminates possible in is allocation of resources as producers use their resources to produce only goods wanted by the societies or consumers, unlike in the socialist economy, where production of goods produced may not be wanted by the people due to poor planning.

DISADVANTAGES OF CAPITALIST ECONOMIC SYSTEM

Exploitation is dominant.

Poor people are de-private of all means of survival and are forced to sell their labor power to the capitalists who exploit them by paying them with low wages.

It leads to the economic and social crisis.

The economic system is not planned as the result it is frequently affected by economic instabilities like inflation, depression, over production, unemployment etc.

It leads to wastage of resources.

Extreme competition behaviors of firms results in misapplication of resources, hence overproduction or harmful production etc.

If leads to distortion in consumer’s choices. Consumer’s choices may be distorted by persuasive advertising, in which consumers may buy commodities of sub-standard due to the convincing power of the suppliers i.e. through under advertisement.

Welfare of the majority is endangered.

Firms under this system compete to maximize profits. Under profit motives they often use resources to produce luxury goods instead of public goods. E.g. health services, education, e.t.c, which promote the living standard of people.

Existence of classes.

That is the rich and poor classes. The classes exist due to unequal access to the major means of production.

MIXED ECONOMIC SYSTEM

Mixed economic system refers to the type of economic system which involves both public and private ownership of the major means of production like capital, land and other related means of production.

Therefore decisions on important economic issues involve some forms of planning by private as well as public enterprises and interaction between the government business and labor through market mechanism.

FEATURES OF MIXED ECONOMIC SYSTEM

Some resources are owned by individuals and some are owned by government.

Decisions regarding production. The production of commodities is partly made by individuals and partly by the government.

There is joint venture in the ownership of business firm. The government tends to have shares with the private investors in running businesses. e.g. TBL in Tanzania.

The role of the government is to regulate the private sector to work for national interests and not for their personal interests.

There is a system of price mechanism and planning authority. All are important in economic decisions and planning.

There is a relative high freedom of choice for both consumers and producers.

ADVANTAGES OF MIXED ECONOMIC SYSTEM

The system is effective in controlling market failure, since the price mechanism does not efficiently provide public goods like education, health, road, etc. The government corrects the weaknesses by providing free goods.

Control of efficiency in production and wastage in the allocation of resource. The system involves some kind of planning in the case it can control wastage of resources also increase of freedom in allocation of the resources competition which also increases efficiency in production.

Classes are minimized as the state take cares of the under privileged by redistributing wealth in the economy.

There is wider freedom.

A private sector is allowed to produce goods and services that give consumers wider range of goods and services to consume unlike in pure socialism.

THE ROLE OF THE GOVERNMENT IN MIXED ECONOMIC SYSTEM

To establish the framework of rules and regulations.

To re distribution income. That is to reduce the gap between the rich and poor. E.g. high taxation, subsidization etc.

To maintain laws and orders in the economy.

To promote high rate of economic growth and economic development.

To stabilize price in the case of inflation or deflation.

To provide public goods such as;-education, health and other related public good

THE TRANSITION PERIOD

Definition: a transition period is the period between any two economic systems such that one system (the old system) is being replaced by another system (the new system).This means that the economic system has not completely collapse yet and the new system is just in the process of being established

It is a period which is characterized by the remnant features of the old economic system and the new features of the new economic system. For example;-before socialism was not well established in Russia element of capitalism were not completely wiped out in the young socialist economy

IMPORTANCE OF THE TRANSITION PERIOD

It is the period of making adjustments. That is it is a period when the weakness of the old system should be left out and the good element of the old system should be in the new system

It is a period of learning from the experience of other economic system in the past and present in order to determine their weakness and strengths

It is the period experimenting on how the new ideas will be introduced and how these ideas will be accepted by the general public

It is a period of action and seriousness with the aim of achieving the predetermined goals/objectives

The transition period is necessary since it is a period of making the society aware of intended objective change and how these changes will be made.

...

No comments:

Post a Comment